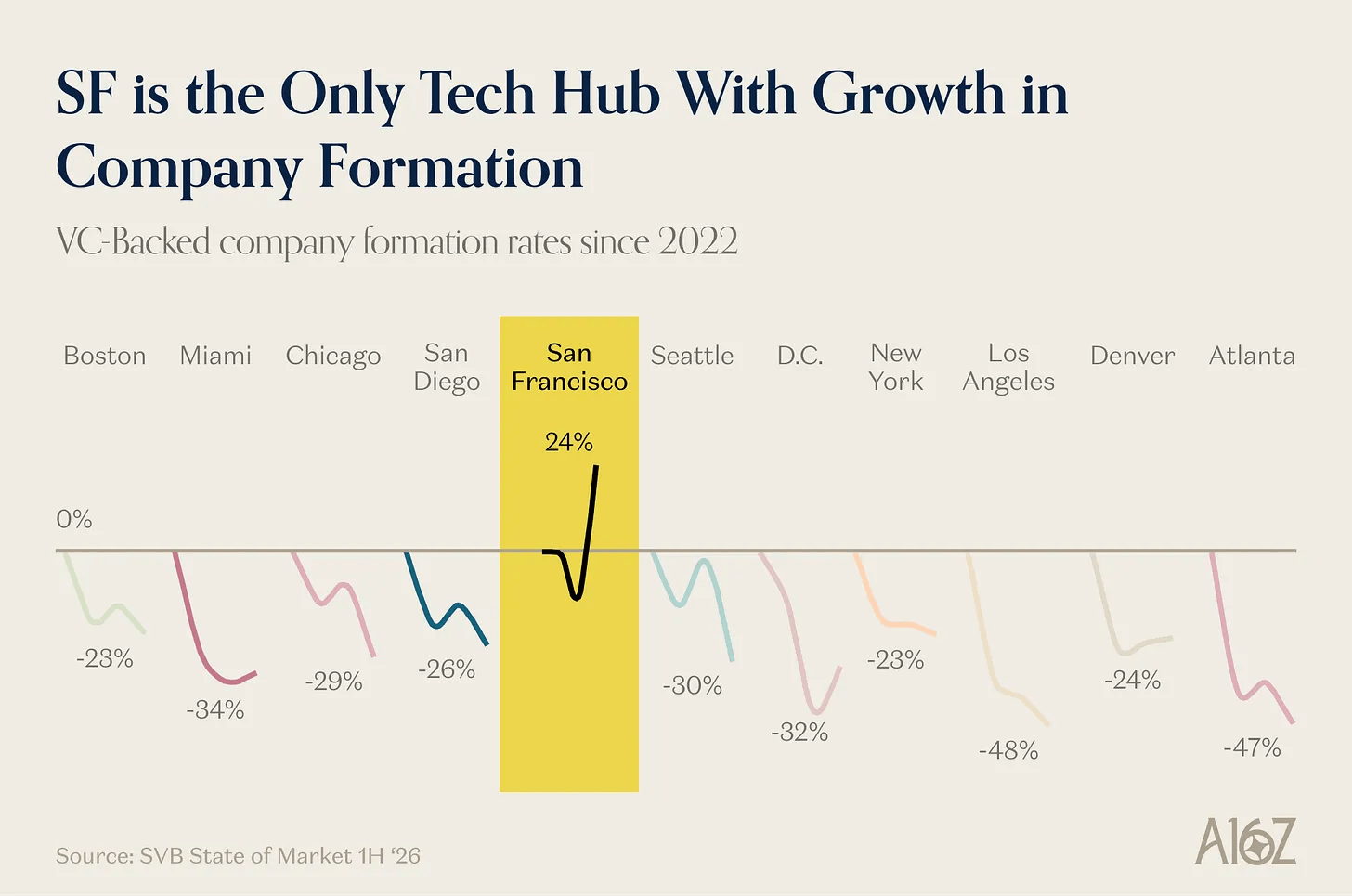

Silicon Valley Bank recently published a report analyzing the growth and decline of VC-backed startups since 2022 across the largest metro regions in the United States. Using 2022 as the baseline year, the data shows that, across nearly every major market outside the San Francisco Bay Area, the number of newly VC-backed startups has dropped sharply. In places like Atlanta and Los Angeles, the number is down nearly 50 percent.

What happened?

Here are a few perspectives.

1. The hangover from 2020 and 2021

During the depths of COVID, tech startup valuations surged. As millions of people shifted to remote work, capital poured into productivity tools and software for laptop-based workers. Combined with near-zero interest rates, this created a speculative environment where significant amounts of capital were invested at valuations that, in hindsight, were not sustainable.

When interest rates rose and liquidity tightened, growth rates slowed. Public market valuations declined, which forced a reset in private markets. Many startups that raised capital during that period found themselves overvalued relative to new market conditions. Venture funds from that vintage are, in many cases, still underwater.

As a result, venture capital firms slowed their pace of investment, and limited partners reduced allocations to the asset class. Given those dynamics, a decline in newly VC-backed startups was inevitable.

2. AI investments crowding out everything else

On November 30, 2022, ChatGPT was released, marking a clear inflection point. It was both an “aha” moment and the beginning of a new technology cycle centered on artificial intelligence.

The implications for legal services, finance, healthcare, software development, research, analytics, and virtually every other knowledge-based profession became immediately apparent. Venture capital and corporate investment dollars shifted aggressively toward AI. The center of gravity returned to San Francisco, where much of the foundational AI work was concentrated.

Capital that might have gone to traditional SaaS and productivity startups instead flowed into AI infrastructure, foundation models, and experimental prototypes. Expected growth in traditional SaaS segments failed to materialize. As AI capabilities advanced faster than anticipated, even more capital followed.

Today, a meaningful share of economic growth is tied to AI-related investment, including data centers, GPUs, specialized chips, power generation, and cooling infrastructure. In this environment, non-AI startups are competing for a shrinking pool of venture dollars. AI has crowded out a substantial portion of traditional venture-backed startup formation.

3. Public software company valuation resets

As AI has improved, particularly in areas like code generation and software development, the perceived terminal value of many traditional software businesses has come under pressure. Barriers to entry are lower. New competitors can be launched more quickly. At the same time, companies expect to achieve greater productivity with fewer employees, slowing seat-based SaaS expansion.

The net effect is that public software company valuations are down significantly from their highs. When public multiples contract, private market valuations must adjust as well.

If a startup raised its last round at 10x revenue and the market now supports 5x revenue, management teams are understandably reluctant to raise capital at a lower valuation. Instead, many choose to conserve cash and attempt to grow into a stronger valuation. Venture capitalists, closely tracking public market comparables, are also less willing to pay premium valuations for non-core AI startups. This often results in a valuation impasse. Fewer deals get done, and fewer startups are newly VC-backed.

The broader perspective

The most important reminder when reviewing the SVB data is that the vast majority of startups are not venture-backed and never will be.

Startup activity itself remains strong. It has never been cheaper to build a product. The tools available to founders, especially AI-driven tools, dramatically lower the cost of experimentation and iteration. Robotics and intelligent hardware are also emerging as significant long-term trends.

We are at the beginning of another innovation cycle. Venture capital plays a role in a small fraction of startup formation. While VC is still digesting the excesses of the COVID-era bubble and concentrating capital in AI, particularly in large foundation model companies, entrepreneurship more broadly is alive and well.

The number of newly VC-backed startups may be down. The number of new startups, however, is not. The long-term outlook for builders remains bright.

Leave a comment