Recently, I was meeting with an entrepreneur who lamented that they weren’t making much progress in their startup. My immediate response was simple: every bit of effort helps.

The crazy thing about startups is that, in the early days, you never know when the breakthrough will come. One more meeting. One more phone call. One more feature. One more introduction. While progress often feels incremental, it really is a leap of faith that the pieces will eventually come together and things will work out.

One of my favorite phrases about entrepreneurs getting started is that you have to be blissfully ignorant of the challenges and difficulties of building a successful business. It is astronomically hard to get a novel idea off the ground. Yet it has always been that way, and it is exactly what it takes to move the world forward.

Another phrase I like is that you just have to put one foot in front of the other. The idea is simple: keep going and keep moving, even when you don’t know exactly how you are going to get there. What you do know is that progress requires effort, and every bit of effort helps.

One of the best things an entrepreneur can do is find a group of like-minded founders at a similar stage and meet with them regularly, whether weekly or monthly. There is something powerful about being in the grind with a group of peers that makes it slightly easier to push forward in the face of adversity. With a peer group comes accountability, shared experience, and camaraderie as you navigate the high highs and low lows of entrepreneurship. Many founders create their own groups of peers or join organizations like Entrepreneurs’ Organization or Young Presidents’ Organization. Either way, a peer group helps sustain the effort.

Being an entrepreneur really is one of life’s great challenges. Getting a business off the ground, signing the first customers, and building the product all require leaps of faith. But like anything important in life, every bit of effort helps.

As the founder of Southwest Airlines, Herb Kelleher, once said: “I have a strategic plan. It’s called getting things done.” Turn effort into results, and results into startup success.

Last week, I gave a talk at a conference. After the event, a gentleman came up to me and started asking about the local startup community. After going back and forth for a bit, it became clear that he was interested in angel investing.

He then shared that he had already made 15 angel investments over the past several years, and every single one of them had gone to zero. Worthless. He participated through local angel investment groups. It wasn’t him running around by himself writing checks. Like many of us are told, he diversified. He made a number of investments with the expectation that one would perform exceptionally well and make up for the losses of the others.

But here he was, after 15 investments and all failures.

Reflecting on his story, I’m sure he’s not alone. I’m certain there are many others who have made that many angel investments and seen them all fail. We know that the vast majority of startups fail. We know that 99% of startups never achieve $1 million in revenue. With those kinds of statistics, it makes sense that there’s a meaningful probability that 15 angel investments could produce zero winners.

So what should someone do?

Number one: invest with a local venture fund. Become a modest limited partner in a reputable local venture fund. Use the experience to understand how they select entrepreneurs and evaluate startups. Spend time with the portfolio companies and look for ways to add value. Then consider participating in select follow-on rounds for the startups you believe in most.

Number two: invest when there is an experienced lead. If a successful angel or venture capitalist is leading the round, the odds improve. Experienced investors have pattern recognition. They have seen what works and what does not work. The biggest challenge for first-time angels is what I call the “leftovers law.” After deals have been shopped around to professional investors and experienced angels and everyone has passed, they often make their way to newer angels who are eager to get started. Frequently, there is a reason others declined.

Number three: invest in areas where you have unique expertise. Many angels I meet want to invest in tech startups but do not actually work in the tech industry. They come from law, medicine, finance, or real estate and want to dabble in tech because it sounds exciting. It is often far better to invest in startups within your own domain of expertise, where you have a genuine informational or network advantage. Invest in what you know, not what sounds cool.

Overall, my goal is not to dissuade new angel investors. Entrepreneurs need capital, mentors, and advisors, and angels often serve as all three. My goal is to help angel investors increase their odds of success so they continue investing and build long-term relationships with entrepreneurs.

The great thing about startups is that this is not a zero-sum game. The more innovation and invention we create, the better off everyone is. We need to invent the future, and angel investors are an important part of that ecosystem.

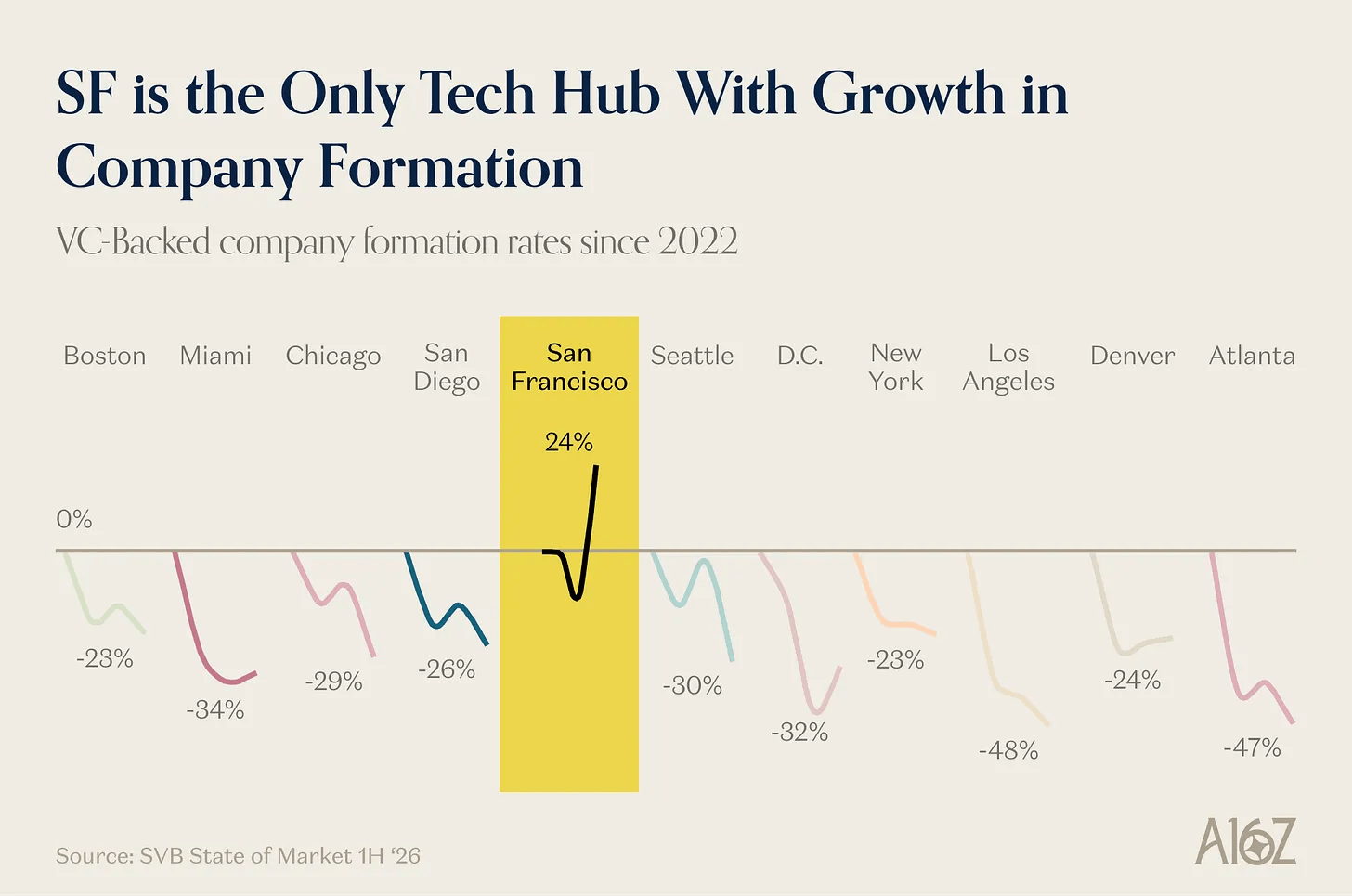

Silicon Valley Bank recently published a report analyzing the growth and decline of VC-backed startups since 2022 across the largest metro regions in the United States. Using 2022 as the baseline year, the data shows that, across nearly every major market outside the San Francisco Bay Area, the number of newly VC-backed startups has dropped sharply. In places like Atlanta and Los Angeles, the number is down nearly 50 percent.

What happened?

Here are a few perspectives.

1. The hangover from 2020 and 2021

During the depths of COVID, tech startup valuations surged. As millions of people shifted to remote work, capital poured into productivity tools and software for laptop-based workers. Combined with near-zero interest rates, this created a speculative environment where significant amounts of capital were invested at valuations that, in hindsight, were not sustainable.

When interest rates rose and liquidity tightened, growth rates slowed. Public market valuations declined, which forced a reset in private markets. Many startups that raised capital during that period found themselves overvalued relative to new market conditions. Venture funds from that vintage are, in many cases, still underwater.

As a result, venture capital firms slowed their pace of investment, and limited partners reduced allocations to the asset class. Given those dynamics, a decline in newly VC-backed startups was inevitable.

2. AI investments crowding out everything else

On November 30, 2022, ChatGPT was released, marking a clear inflection point. It was both an “aha” moment and the beginning of a new technology cycle centered on artificial intelligence.

The implications for legal services, finance, healthcare, software development, research, analytics, and virtually every other knowledge-based profession became immediately apparent. Venture capital and corporate investment dollars shifted aggressively toward AI. The center of gravity returned to San Francisco, where much of the foundational AI work was concentrated.

Capital that might have gone to traditional SaaS and productivity startups instead flowed into AI infrastructure, foundation models, and experimental prototypes. Expected growth in traditional SaaS segments failed to materialize. As AI capabilities advanced faster than anticipated, even more capital followed.

Today, a meaningful share of economic growth is tied to AI-related investment, including data centers, GPUs, specialized chips, power generation, and cooling infrastructure. In this environment, non-AI startups are competing for a shrinking pool of venture dollars. AI has crowded out a substantial portion of traditional venture-backed startup formation.

3. Public software company valuation resets

As AI has improved, particularly in areas like code generation and software development, the perceived terminal value of many traditional software businesses has come under pressure. Barriers to entry are lower. New competitors can be launched more quickly. At the same time, companies expect to achieve greater productivity with fewer employees, slowing seat-based SaaS expansion.

The net effect is that public software company valuations are down significantly from their highs. When public multiples contract, private market valuations must adjust as well.

If a startup raised its last round at 10x revenue and the market now supports 5x revenue, management teams are understandably reluctant to raise capital at a lower valuation. Instead, many choose to conserve cash and attempt to grow into a stronger valuation. Venture capitalists, closely tracking public market comparables, are also less willing to pay premium valuations for non-core AI startups. This often results in a valuation impasse. Fewer deals get done, and fewer startups are newly VC-backed.

The broader perspective

The most important reminder when reviewing the SVB data is that the vast majority of startups are not venture-backed and never will be.

Startup activity itself remains strong. It has never been cheaper to build a product. The tools available to founders, especially AI-driven tools, dramatically lower the cost of experimentation and iteration. Robotics and intelligent hardware are also emerging as significant long-term trends.

We are at the beginning of another innovation cycle. Venture capital plays a role in a small fraction of startup formation. While VC is still digesting the excesses of the COVID-era bubble and concentrating capital in AI, particularly in large foundation model companies, entrepreneurship more broadly is alive and well.

The number of newly VC-backed startups may be down. The number of new startups, however, is not. The long-term outlook for builders remains bright.

AI—and how to get real value from it—is one of the hottest topics in startup land right now. Entrepreneurs have been sharing how they’re incorporating it into their businesses in ways that go far beyond the basics.

By now, we’ve all used LLMs for research, summaries, and content production. Those use cases are powerful—but they’re just the beginning. Coding companions and “vibe coding” have received most of the attention, deservedly so. Still, even for non-developers, there are more advanced AI tools that should already be part of the workflow. Here are a few I’ve been experimenting with:

1. Open-source AI as an employee For the past few weeks, I’ve been using OpenClaw, an open-source agent running on my Mac Mini, prompting it to create software, conduct longer-running research, and act as an assistant. The big idea is simple: treat the AI like an employee. Give it access to your corporate tools and a full web browser, and there’s no reason it can’t handle a significant percentage of the tasks knowledge workers typically do.

2. Spreadsheet and financial model work AI tools are now incredibly strong at building financial models, writing scripts for data transformation, and running complex analyses. Instead of delegating the first draft of an analysis to someone on your team, try doing it yourself—with AI as your partner. Force yourself to use AI to accomplish the goal and see how far you can get. You may be surprised by how much leverage you already have. Start with Gemini for Google Sheets or a similar tool.

3. A coworker agent as your default mode Run through a coworker-agent tutorial like Claude Code for Everyone and then use it as your default operating method for the day. Let it draft emails, summarize documents, analyze data, and plan tasks. It won’t be perfect, and it won’t finish everything. But by making it your starting point—and cleaning up around the edges—you’ll quickly appreciate what’s already possible. The productivity gains are real today, and the software will only continue to improve.

There’s also a growing debate about AI eliminating “laptop jobs.” I’m in the camp that believes higher productivity ultimately increases demand for capable team members. Historically, the diffusion of new technology takes longer than people expect. The world will absolutely change—but it’s unlikely to result in mass unemployment in the next 12 to 24 months. Over the next decade, we’re far more likely to see a productivity boom that enables people to do more meaningful work at greater scale and make a larger contribution.

Entrepreneurs should deeply integrate advanced AI tools into the workflow of every team member. If someone isn’t willing to adopt them, that’s a real issue. The companies that fully embrace these tools will move faster, learn faster, and compound progress more quickly.

It may feel uncomfortable at first. But over time, founders and teams who put AI at the center of their workflow will increase their velocity and accelerate progress toward their vision.

Don’t wait. Make AI foundational—personally and across your startup.

One of the most talked-about trends right now is the rapid decline in software-as-a-service valuations. Public markets in the sector have fallen dramatically over the last few weeks. Strong SaaS companies that were previously trading at seven to eight times revenue are now often trading at three to four times revenue.

Why is this happening? Let’s look at the main reasons being discussed.

1. AI coding tools enable “vibe coding.” AI coding tools make it easy to build your own software. You can simply talk to a computer and it will create new software to replace existing SaaS applications. Don’t like your CRM? Vibe-code a new app that does exactly what you want.

2. Software lock-in is disappearing. AI tools are extremely good at manipulating data and converting it between systems. In the past, SaaS businesses benefited from a premium valuation because switching costs were high. Now, AI makes it much easier to move between vendors, eroding that lock-in.

3. Per-seat SaaS pricing is under pressure. Most SaaS products are priced per user, per employee, or per seat. In the age of AI, a single AI agent can effectively act as a “seat” and do the work of dozens or even hundreds of humans. Combined with companies having fewer employees and pushing for higher productivity, the ability to sell more seats is significantly diminished.

4. Long-term revenue durability is less certain. Historically, it was easy to assume that SaaS products, especially platforms of record, would have 20- to 30-year longevity. While short-term durability may still exist, long-term durability is now more questionable. If future cash flows are less certain, company valuations should decline accordingly.

5. Customers don’t need all the functionality—and can’t unbundle pricing. A friend recently shared a story about paying six figures annually for a product with extensive functionality, when they only needed a small slice of it. There were no lower-cost or modular options. Instead, they vibe-coded the specific functionality they needed in a single weekend and chose not to renew their contract. Many SaaS products are comprehensive, but their pricing and packaging are not agile enough for this new reality.

6. Barriers to entry are near zero. AI coding tools dramatically reduce the cost of building new products. Tens of thousands of new SaaS applications are being created with cost structures that are a fraction of incumbents. Even if companies don’t build their own tools, they can increasingly find alternatives in the market at one-tenth the price.

7. Value is being captured by AI platforms. As SaaS products are reduced to services, data stores, or systems of record, AI platforms layered on top will capture most of the net new value. Customers may receive more value overall, but traditional SaaS applications will capture a smaller share of incremental spend.

SaaS valuations have been under pressure for some time, particularly after the bubble of 2020 and 2021. The last few weeks have been especially dramatic and may represent an overcorrection. Even so, the valuation landscape for SaaS has changed permanently.

For these reasons and others, the future of SaaS fundraising and valuations will likely be more modest on a long-term basis. Entrepreneurs would do well to embrace this disruption: build AI-first SaaS companies with low cost structures, flexible pricing and packaging, and a focus on solving the hardest customer problems at dramatically lower cost.

The future is not fewer SaaS products—it’s ten times as many. And wherever there is opportunity, entrepreneurs will step in to fill the void.

Last week I had a great conversation with a group of entrepreneurs, and our first topic was identifying each startup’s North Star metric. A North Star metric is the single most important metric in a business—the one that best captures customer value, reflects what is going well, and creates a singular focus for continually improving the company.

The most common answer when you ask an entrepreneur about their most important metric is revenue or annual recurring revenue. While these are critically important, they are outcomes of customer value, not the value itself. The better question is: what is the specific thing customers do where value is most clearly created? What action best represents real benefit from using the product?

When I posed this question to the group, one underlying theme emerged: many founders started with a vanity metric because it felt like a quick and easy way to measure progress. A classic example of a vanity metric is page views inside a web application. Usage can be a proxy for value, but merely clicking around is not the same as achieving a meaningful result with the product.

Once you decide on your North Star metric, the next step is to embed it everywhere. Put it on a big screen in your lobby. Include it in your weekly email updates. Make it the headline metric in your quarterly board deck. Align company goals and initiatives around it. Make sure every employee understands how their work contributes to it.

A simple test of alignment is to ask any employee, “What is our North Star metric, and how are we doing?” If they can’t answer clearly, your communication around it has been insufficient.

Entrepreneurs, my recommendation is this: choose a North Star metric that truly represents the value you deliver, track it rigorously, and ensure your entire team rallies around it. A startup is more than a single metric, but there is nothing more powerful than clarity about what you are working toward and why.

Software-as-a-service valuations have been in the doldrums for several years. After the peak hype of 2020–2021 and the COVID-fueled pull-forward of demand followed by the end of the zero-interest-rate era, SaaS valuations have been under consistent pressure.

If you read commentary online and talk with entrepreneurs and investors, three main explanations usually come up.

First, AI investments have sucked much of the oxygen out of the room. On both the entrepreneur side and the corporate buyer side, there is simply less capital available to invest in traditional business productivity software.

Second, valuations for tech companies are still primarily driven by growth rates. With growth rates down dramatically—whether due to increased AI spending, fewer employees (since most SaaS products are priced per seat), or other factors—high valuation multiples are difficult to justify. Without high growth, you are not going to get high multiples.

Third, and possibly the most disruptive argument, is the rise of “vibe coding” and tools like Cursor for developers, and Replit and Lovable for building custom applications through simple prompting. The idea is that companies will increasingly build their own internal software rather than pay $100 per user per month for generic tools, when they can build exactly what they want and customize it as their needs change.

This feels far-fetched once you consider how complicated edge cases and real-world nuance become beyond surface-level CRUD apps. Yet here we are, and these are the arguments being made.

What’s missing from the conversation is another explanation—one that is likely the biggest long-term challenge and is closely related to the third point. While some companies will indeed build their own internal tools, I believe the much larger threat to incumbent SaaS companies is the rise of new SaaS startups created by non-technical subject-matter experts.

As the cost of building software approaches zero and the cost of hosting software on cloud infrastructure enables near-infinite scalability in line with customer growth, the barrier to creating new SaaS companies has never been lower. Instead of paying $20,000 per year to an incumbent vendor, why not pay $2,000 per year to a new SaaS company that delivers 90 percent of the functionality at 10 percent of the cost?

These new companies do not have large customer bases that slow down product development. They do not have immense pressure from existing investors and financial partners. In many cases, everything will be AI-native. The era of a few hundred thousand dollars of recurring revenue per employee may be coming to an end. No technical debt. No outside pressures. Just high-quality, vibe-coded software built by small teams that orchestrate it, and customers who love getting more value for their money.

Entrepreneurs looking for new ideas should lean directly into this. They should find the most unloved SaaS software they can and vibe-code their way into a new entrant in that market, grinding away to create a product customers love that delivers maximum value for minimal cost. It will not be glamorous, but I am confident thousands of entrepreneurs will do exactly this and build strong small businesses.

Incumbent SaaS companies are already under tremendous valuation pressure, and things are only going to get more challenging as a Cambrian explosion of vibe-coded SaaS applications comes online.

Last week I was talking with a board member about how to be helpful to an entrepreneur we both know. A few minutes into the conversation, the board member said, “We need to get him from being a 10/90 entrepreneur to a 90/10 entrepreneur.” I had never heard this phrase before, so I asked for clarification. He explained that a 10/90 entrepreneur spends 10 percent of his time on the most important things and 90 percent on the less important things. From his perspective, we needed to help the entrepreneur reorient how he thinks so he could become a 90/10 entrepreneur, spending 90 percent of his time on the most important priorities and only 10 percent on activities that don’t add as much value.

After he said this, it struck me how common this pattern is in the entrepreneurial world. Human nature pushes us to focus on whatever is right in front of us, whether it’s busywork, an annoyance, or something that can be handled immediately. For entrepreneurs, a real shift in mindset has to take place. Just because you can do something doesn’t mean you should do it.

When I was in college, our economics textbook used a popular example to explain competitive advantage versus comparative advantage. At the time, Michael Jordan was the most famous athlete in the world, and the example suggested that he might be the best and fastest lawn mower on the planet. Even if that were true, mowing lawns would not be where his greatest value lies. His value is in playing basketball, so that’s where he should spend his time. The same principle applies to entrepreneurs.

Of course, in the early years most entrepreneurs don’t have this luxury. There is a period when you have to do whatever it takes to keep the lights on, including the most basic and mundane tasks. I personally spent years doing exactly that. Once we reached some modest scale, it required a huge rewiring for me to delegate responsibilities and find great people who were better at many of those tasks so I could focus on where I could contribute the most.

Entrepreneurs would do well to think intentionally about the journey from 10/90 to 90/10 and to develop the discipline and prioritization needed to spend the majority of their time on the areas where they are most uniquely skilled and suited. The path from 10/90 to 90/10 is often bumpy, but the entrepreneurs who grow and develop faster than their startups ultimately achieve the greatest success.

Last week I was catching up with an entrepreneur who told one amazing story after another. When I left the conversation, I could not stop thinking about how impressive his storytelling ability was. It made me reflect on the power of stories and how entrepreneurs should lean into them and deliberately work to get better, especially if it does not come naturally.

Many entrepreneurs are visionaries, dreamers, and big-idea thinkers. But there are also plenty of engineers and logic-driven founders who prefer dealing in facts rather than stories. I fall into that nuts-and-bolts camp myself, which means I have to work at storytelling.

Like any skill, storytelling can be improved with practice. Whenever I hear an interesting anecdote, a witty saying, or a compelling quote, I save it in a note on my iPhone. With a quick voice dictation, it is captured in seconds and stored indefinitely. Using the same approach, it would be easy to record a story or anecdote every day. Over time, you build a personal library you can draw from in future conversations.

The real challenge is forming the habit. Do you spend ten minutes each morning reviewing the prior day for stories worth saving? Or do you train yourself to capture them the moment they happen? The best storytellers seem to do this naturally. They have an almost unbelievable ability to recall the right story on demand. Even without that natural talent, a simple, lightweight system can dramatically elevate your storytelling.

Humans evolved around campfires, sharing stories for thousands of years. The power of a story is unlike anything else. My recommendation for entrepreneurs is to exercise their storytelling muscle and actively look for ways to improve their craft. Writing, speaking, and every other form of communication becomes far more powerful when driven by compelling stories.

With the new year upon us, it is a great time to reflect on last year’s accomplishments and set new goals for the year ahead. As I read various “lessons learned” articles and annual recaps, I often think about what my single most important piece of advice for entrepreneurs would be.

Advice is extremely stage- and journey-specific. Many entrepreneurs consume a wide range of guidance that is simply not applicable to their situation. It may be too big, too small, too early, too late, or designed for an entirely different type of market. It is always important to understand the background of the person giving the advice and who it is really meant for.

That said, my number one piece of advice for entrepreneurs in the new year is simple: write and send a weekly or monthly update to anyone who cares about what you are doing.

This could include employees, advisors, investors, mentors, family members, friends, or fellow entrepreneurs. Who receives it matters far less than the fact that you do it consistently. Ideally, you set aside 30 to 60 minutes each week to write down what you accomplished last week, what you are working on this week, your main goals for the quarter and the year, your top priorities, and any specific asks, such as introductions, advice, or feedback.

This update should be a recurring event on your calendar. Each one can live in its own Google Doc and be sent to a BCC list maintained in a simple Google Sheet. You can certainly use email marketing software or a dedicated app, but I recommend starting with this straightforward, brute-force approach and adding tools later if needed.

Writing this regular update is incredibly valuable for your own clarity. It forces you to organize all the ideas swirling in your head, the highs and lows, and the messages you want to communicate. At the same time, it is one of the best ways to keep your network informed and to make it easy for them to help you.

Entrepreneurship is filled with extreme highs, deep lows, and long stretches of wandering in the desert. A recurring written update brings clarity, both internally and externally, through that entire journey. As a bonus, after years of doing it, you end up with a detailed journal of your entrepreneurial life that can one day become a book or something you pass down to your children and grandchildren.

My recommendation is simple: send a weekly or monthly update email. Include anecdotes, metrics, projects, and the things you need help with. Make it a habit, and make sure your audience receives it at the same time every week or month.