Over the years, I’ve debated the pros and cons of venture debt with a number of people. Some entrepreneurs see venture debt as a safety net, with a big “Do Not Break Unless Emergency” sign in front of it. Other entrepreneurs view venture debt as a way to grow the business faster with minimal or no dilution.

During the Pardot days, we had a scalable business model and used venture debt to grow faster as part of our capital-light strategy. Our first line of venture debt was $1.5 million, and as the business grew, we secured a new line of credit for $3 million. By the time of our sale, we had used almost all of our debt capital in an effort to keep up with the market. It was the right thing to do for the business.

For Salesloft, the company raised several rounds of equity financing and increasingly larger venture debt lines of credit due to continual access to equity from institutional investors. Venture debt was primarily viewed as a safety net. When COVID hit in March 2021, we pulled down the line of credit, not knowing if it would be needed. In the end, it wasn’t, but it provided a cash cushion in case the COVID shock persisted.

This backdrop provides context for the announcement of our new private credit fund for growth-stage startups called Conductor Capital. The founders, Zack Mansfield and Dhruv Patel, have been in the venture debt world for many years, working for bank departments that specialize in startups. Many years ago, one of Zack’s clients was, in fact, Salesloft. Personally, I’ve written about venture debt many times and have used it in several startups (here, here, here). With Silicon Valley Bank, First Republic, and others going under last year, it was clear a gap had emerged in the market to help startups through venture debt.

Last year, after personally talking to several entrepreneurs about doing something on our own in the private credit space for startups, Zack reached out, saying he was working on a new firm. We began discussing the idea and decided to launch a new private credit fund focused on tech startups, called Conductor Capital. To support Zack and Dhruv, we recruited Kyle Porter from Salesloft, Tope Awotona from Calendly, and Nat Turner from Flatiron Health/Collectors. The big idea is: capital from entrepreneurs to support other entrepreneurs.

Today, we’re investing out of our first fund and have already closed our first loan.

Congrats to Zack and Dhruv on the launch, and please consider Conductor Capital when evaluating venture debt options. Conductor Capital is open for business.

Last week, I was catching up with an entrepreneur who shared a concept with me that I hadn’t heard before: negative roadmaps. In the startup world, a product roadmap outlines the features and functionality expected over the next few quarters or years. The idea with a traditional roadmap is to set a vision and direction for the product. By doing so, it helps sell to potential prospects what’s coming down the pipeline, share with existing customers where you’re going from a technology point of view, and align the internal team around priorities for engineering and product development.

Of course, entrepreneurs are an optimistic bunch and often want to be helpful to as many people as possible, which can lead to broad roadmaps or products that are overly expansive. One of my early lessons, learned many years ago, was specifically around this issue. We had a successful product, and we were growing nicely, but I fell into the trap of trying to be all things to all customers, both current and future. After building out a bunch of features and seeing that they weren’t being used much, I still tried to continually enhance the product. However, this only slowed down development because more code, technical debt, documentation, and training were required.

I realized that from a roadmap perspective and in feature development, it’s incredibly important to have an opinionated vision of where you’re headed. That opinionated vision from a product point of view doesn’t necessarily include all the existing customers you have today. The customers you want to have tomorrow may vary slightly or could be at the high or low end of the market. The idea is that the roadmap and the opinionated vision of the future should reflect what you want to have, not necessarily what you have today—although they could be one and the same.

The idea I learned about last week is that a negative roadmap. A negative roadmap tells you what you’re not going to do in the future. For example, it might outline feature requests we’ve received over the years that we’re not going to implement, modules customers have asked for that we are not going to build, or types of functionality that competitors offer but don’t align with our ideal customer profile, so we won’t implement them.

This idea of a negative roadmap is complementary to the normal roadmap. It’s a way to document things that are not going to happen in the product or things that are going to be removed from the product. Roadmaps are critically important, and as organizations grow, getting everyone on the same page becomes harder. Adding a negative roadmap to the mix is another exercise in aligning the team around what is not going to happen. Entrepreneurs should consider adding a negative roadmap to their collection of documents and best practices that they use to run their startup.

Last week’s post on the Atlanta companies in the Inc. 5000 awards highlighted one of our very own, Intown Golf Club, at Number 204. After reading about this award, several friends reached out with comments and congratulations. After all the feedback, I decided it would be a good time to share our origin story and progress on the business.

Back in 2018, I installed a new golf simulator in my basement garage. It was simple and not too fancy—a net return with a hitting mat, combined with a Foresight launch monitor attached to a laptop. I was convinced that with a simulator, I could become a scratch golfer. I quickly learned otherwise, but that’s a different story.

After using the simulator regularly for a few months and having friends and family try it out, the proverbial lightbulb went off. This is an amazing piece of technology that requires a large room, tall ceilings, and cumbersome equipment, making it difficult for most people to install in their homes. Why isn’t there a chain or franchise of great indoor golf clubs around the country? In places like South Korea, there are thousands of indoor golf facilities, yet in the United States, they are almost nonexistent, except for simple setups by golf teaching pros to sell lessons. It’s tons of fun to hit on the simulators, playing different games for kids, running various combine test sessions, and, of course, playing golf courses like Pebble Beach and Killearn.

After thinking about it for a bit, I shared the concept with Jon Birdsong to get his ideas. He hadn’t used a simulator in a long time, and in the interim, the technology had improved dramatically. Once he experienced the latest equipment, he became convinced there was something to this indoor golf club concept. Jon, I, and several friends had been batting around the idea for a while when we were at lunch at Jack’s Deli near the Atlanta Tech Village. In walks Michael Williamson, a fellow tech entrepreneur who had been at ATV for many years and had recently sold his software company. Knowing that Michael loved golf as well, we asked him when was the last time he hit on a golf simulator. Immediately, he said, “last night while watching the football game.” Little did we know, he had a simulator at his house and absolutely loved it. We pitched the idea of building an indoor golf club starting in Atlanta and expanding nationwide. Michael loved it, and we were off to the races.

Our next major step in the concept was taking one of the large boardrooms in the Atlanta Tech Village and renovating it with a high-end golf simulator, renaming it “Lenox National” as it faced Lenox Road. With Lenox National in place, we started inviting friends, acquaintances, and anyone who would listen over to hang out. We’d hit some golf balls, experience the technology, and brainstorm ideas around building an indoor golf club. After great experiences at Lenox National, it became clear that there was a huge opportunity to build what became Intown Golf Club.

Our next step was finding a great location. We went out to the market and looked at a couple of old restaurant sites on Piedmont Road and a few in the greater Buckhead area. After several months of searching without much luck, we got word that one of the tenants in an amazing space at Two Buckhead Plaza wanted to move out, but they had another year left on their lease. We started spending more time with the landlord, looking for solutions. We finally agreed to terms and were ready to sign a lease when COVID hit in early 2020, and the world shut down. Not knowing when life would return to normal, we paused the lease negotiations.

Several months later, it became clear that things were, in fact, going to return to normal, and we signed the lease to build our first location at 3050 Peachtree Rd. NE. Thanks to a referral from Fred Castellucci, we hired Dan Maas and his team at ai3 as our architects to build out a private high-end, modern indoor golf concept. The space has 10 TrackMan bays, one of which is a True Spec Golf fitting bay, one has Tour Putt, and two of them are oversized with doors and curtains to turn them into private dining rooms. In the center, we have an upscale bar and restaurant, and in the back half, we have a high-end lounge with a fireplace. Outside, we have a patio with large putting green. The TrackMan bays run along the perimeter of the 12,000-square-foot space.

We ended up opening the private club in the spring of 2021, and our timing couldn’t have been better. People wanted to get back together with their friends, and golf, as a game, has a huge, passionate base. In fact, one out of every seven Americans played golf last year. It was an instant success.

Now, running a restaurant, bar, and golf facility is not easy. Everything you’ve heard and read about running a restaurant is true. While we’re far from having mastered hospitality, we’re learning fast and evolving as we go. Fast-forward to today, and we have locations in Atlanta, Georgia; Charlotte, North Carolina; and Columbus, Ohio, along with new locations under construction in Philadelphia, Pennsylvania; Houston, Texas; and Nashville, Tennessee. Our goal is to bring the golf club camaraderie and experience to every major market across the country and eventually the world.

Entrepreneurial ideas often come from the simplest of places, and Intown Golf Club is no different. Congratulations to Michael, the team, and everyone involved in building one of the fastest-growing private companies in the United States.

Every year, I enjoy reading the Inc. magazine’s Inc. 5000 awards. It’s one of the best ways to see what’s trending and popular in the small business world, and you never know which companies might become large breakout successes one day. Specifically, within the Inc. 5000 list, I also enjoy seeing which Atlanta companies are doing the best and growing the fastest. Without further ado, here are the some of the fastest growing Atlanta tech and tech-enabled businesses in the Inc. 5000.

VIVA Finance offers affordable, unsecured personal loans up to $10,000, designed with flexible repayment plans based on employment. They focus on financial empowerment through ethical lending, providing an alternative to traditional credit models.

Fusus offers a real-time intelligence platform that integrates public safety assets for law enforcement and private security. Their cloud-based solutions enhance situational awareness, enabling agencies to monitor and respond to incidents more effectively.

Intown Golf Club – The Private Social Club For Golfers

Intown Golf Club is a private social club for golf enthusiasts, offering an elevated golf experience with world-class food and beverage services. It aims to create a convenient and inviting community for golfers, regardless of weather conditions.

Adtechnacity – The Leading Performance Marketing Solution

Adtechnacity provides performance marketing solutions, focusing on helping businesses navigate the digital landscape through data-driven strategies. The company specializes in optimizing ad spend and improving customer acquisition.

Mile Auto offers a pay-per-mile auto insurance solution designed for low-mileage drivers. The platform provides a cost-effective alternative to traditional car insurance by only charging customers for the miles they drive, making it ideal for those who drive infrequently.

DataSeers offers AI-driven SaaS solutions designed for the banking and payments industry. Their platform enhances compliance, fraud detection, reconciliation, and customer lifecycle management, helping financial institutions automate processes and make data-driven decisions.

Polygon.io provides real-time and historical market data through APIs. The platform is designed for developers and financial professionals, offering standardized data formats, client libraries, and extensive documentation. It aims to modernize access to financial data and supports building trading apps, research tools, and other financial products.

Relay Payments – Fast, secure digital payments for logistics

Relay Payments provides a secure digital payment network designed specifically for the logistics industry. Their platform connects freight brokers, fleets, drivers, and merchants to streamline payments for diesel fuel, lumper fees, scales, truck repairs, and more. By digitizing these transactions, Relay aims to save time, reduce costs, and enhance operational efficiency.

Verusen provides AI-driven solutions for optimizing MRO (Maintenance, Repair, and Operations) inventory and supply chains. Their platform helps organizations reduce costs, mitigate risks, and improve operational efficiency by analyzing data from various systems, identifying redundancies, and streamlining procurement and inventory management processes.

AdvizorPro provides a comprehensive and constantly updated database for RIA (Registered Investment Advisor) firms, financial advisors, and other financial professionals. The platform offers tools for targeted lead generation, CRM integration, and data enrichment, helping asset managers, recruiters, and SaaS companies create accurate and high-quality lead lists to optimize their sales and marketing efforts.

Stord – Make Your Supply Chain A Competitive Advantage

Stord offers cloud supply chain solutions combining software and logistics services. They help e-commerce brands optimize their supply chain for better efficiency, reduced costs, and enhanced customer experiences. Their platform provides a unified view of the supply chain, including order management, inventory tracking, and last-mile delivery, tailored to the needs of omnichannel and DTC brands.

Safely provides short-term rental insurance and guest screening services. Their platform offers protection for property managers and homeowners by covering damages, theft, and liability issues caused by guests, while also ensuring guest reliability through screening. Safely aims to make vacation rental management safer and more secure.

Florence Healthcare – Remote Workflows for Clinical Trials

Florence Healthcare offers a Site Enablement Platform designed to streamline clinical trials by enabling remote collaboration between sponsors and sites. The platform addresses challenges in site start-up, conduct, and closeout by digitizing workflows, enhancing compliance, and reducing bottlenecks, ultimately accelerating the clinical trial process.

Affordable Rooms for Rent, Homes, Weekly Rentals & More

PadSplit offers affordable co-living spaces by renting out individual rooms on a weekly basis. The platform emphasizes flexible stays, fast move-ins, and credit-building opportunities for members. It also provides a streamlined process for finding and booking rooms, aiming to make shared housing more accessible and financially beneficial.

Cove.tool – Expert, Sustainable Building Design Consulting

Cove.tool provides AI-powered architectural and sustainability consulting services, offering advanced energy modeling and performance analysis to optimize building designs. The platform supports architects, engineers, and manufacturers by integrating sustainability into projects, reducing costs, and improving design outcomes. Cove.tool emphasizes transparency, accuracy, and efficiency in helping the AEC industry meet environmental goals.

Connected, Continuous, Insight-driven Multidisciplinary Cancer Care

OncoLens provides a platform for multidisciplinary cancer care that integrates patient data across different systems, enhancing collaboration among care teams. The platform uses AI and machine learning to support clinical decision-making, streamline tumor board processes, and improve patient outcomes. It’s designed to help cancer centers and life sciences organizations manage complex cases and optimize treatment planning.

Groundfloor – Build Wealth with Real Estate Investing

Groundfloor is a real estate investing platform that allows individuals to invest in short-term, high-yield debt backed by real estate. With as little as $10, investors can diversify their portfolios and earn passive income. The platform offers automatic investing options, low barriers to entry, and a focus on providing consistent returns, making it accessible for both new and seasoned investors.

Cognosos offers real-time location intelligence solutions powered by AI and machine learning for industries like logistics and healthcare. Their platform improves operational efficiency, safety, and asset management by providing precise location data and actionable insights. With a focus on easy installation and rapid deployment, Cognosos helps organizations uncover bottlenecks, reduce costs, and enhance overall performance.

PlayOn – The Future of School Athletics and Activities

PlayOn Sports provides comprehensive solutions for school athletics and activities, including digital ticketing, broadcasting, athletic management, and sponsorships. The platform integrates services like streaming through the NFHS Network and digital ticketing with GoFan, aiming to streamline school operations and enhance community engagement in school sports and activities.

IRONSCALES – Email Security Software for Enterprise & MSP

IRONSCALES provides advanced email security solutions using AI to protect enterprises and MSPs from phishing, BEC, ATO, and other email-based threats. The platform automates threat detection and response, integrates phishing simulation training, and offers continuous adaptive learning to enhance overall email security.

Kahua offers construction program and project management software tailored for owners, program managers, general contractors, and subcontractors. The platform enhances collaboration, improves data management, and provides robust tools for handling the entire construction lifecycle from preconstruction to operations, aiming to streamline processes and boost efficiency in construction projects.

MessageGears offers a customer engagement platform that integrates directly with your data warehouse, allowing for seamless cross-channel messaging and real-time personalization. Designed for enterprise brands, the platform eliminates data inefficiencies and enables marketers to deliver highly targeted campaigns without the usual technical limitations.

As a bonus, this list was compiled using ChatGPT. What I did was go to the Inc. 5000 website, copy and paste the URLs of each of the top 22 Atlanta winners into a text document, and then went to ChatGPT. I gave it the following prompt:

I’d like you to visit several websites, pull the page title, and summarize the contents of the homepage. Then output a table that has the following columns: number, website address, page title, and page summary where number is result number (e.g. 1 for the first site, 2 for the second site, etc.)

After answering with the first few results, it asked if I wanted to keep going, and I said, “Yes, please keep going.” Finally, when it finished, I said “Please compile all the results into one large table.” I then copied and pasted that table into this blog post you see above.

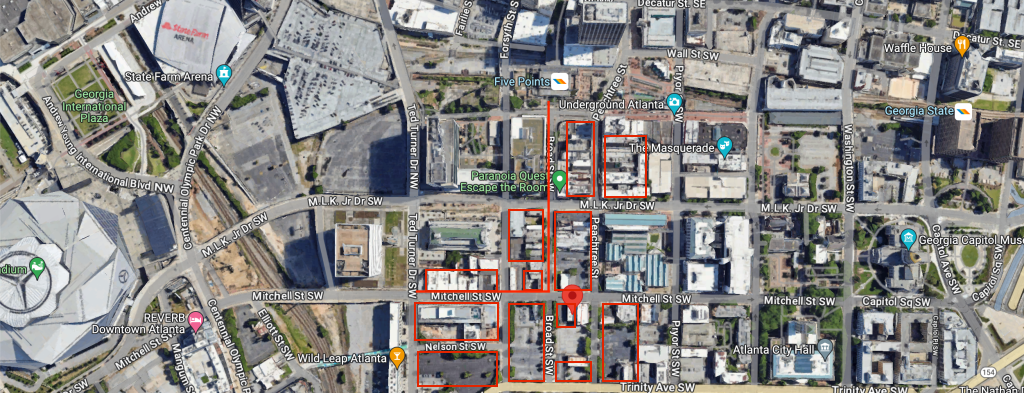

With tremendous support and encouragement following the announcement of Atlanta Tech Village’s expansion to downtown Atlanta, many people have asked how it will actually work in South Downtown. It’s one thing to put a new startup space in one building, but it’s a whole different challenge to take 56 buildings, 11 parking lots, and turn a neglected historic neighborhood into a thriving startup district.

To start, we’ve focused on the core of the neighborhood, which we affectionately refer to as “Elle” as it makes an “L” shape. This path runs from Mercedes-Benz Stadium down Mitchell Street and then up Broad Street to the Five Points MARTA station. Mercedes-Benz Stadium is the most iconic venue in Atlanta, and Five Points MARTA station is the busiest subway station in the city.

Previous developers invested significant capital into Hotel Row, so we’ll begin with a massive 31,000-square-foot Atlanta Tech Village location in one of the buildings closest to Mercedes-Benz Stadium previously known at Hotel Sylvan. Hotel Row will be further anchored by new shops and restaurants. As the neighborhood grows, we’ll continue developing the historic Hotel Scoville building and the historic Concordia building, both on Hotel Row.

ATV Sylvan LoungeATV Sylvan BreakroomATV Sylvan Conf RoomATV Sylvan at 235 Mitchell St

Moving up Mitchell Street from Hotel Row to the center of the neighborhood and the middle block of historic Broad Street, we’ll establish a dozen private offices for founders and creatives. These will be combined with many new restaurants, bars, and stores, anchored by a 15,000-square-foot outdoor town square and the historic HL Green Five and Dime, which will house another 30,000-square-foot Atlanta Tech Village (ATV Green!). Our goal with historic Broad Street is to establish a center of gravity for the neighborhood, with a strong emphasis on community for the startup district.

HL Green as ATV Green

With historic Hotel Row on the southwest side of the neighborhood and historic Broad Street in the center, the area will feature a variety of great startup spaces, food and beverage shops, and a true sense of Atlanta’s history. Hotel Row and historic Broad Street represent 22 of our buildings.

Looking at it on a map, you can see dozens of our buildings north of historic Broad Street and a number of buildings and large parking lots south of historic Broad Street. North of historic Broad, buildings like the original Rich’s Department Store at 82 Peachtree will become incredible loft apartments. The original Bass Dry Goods building at 85 Peachtree, along with the Kress building at 69 Peachtree, are perfect for adaptive reuse. And the list continues. Southeast of historic Broad, the Bass Furniture Building at 142 Mitchell is another beautiful adaptive reuse building. And lastly, directly across from Hotel Row, the large C&S Bank building at 222 Mitchell is another excellent project.

Finally, the many acres of empty parking lots provide decades of new development opportunities to bring more housing to the neighborhood. When finished, it’ll be a complete live/work/play startup district.

The heart of the South Downtown Atlanta startup district is Hotel Row and historic Broad Street, with dozens of startup/creative spaces combined with local restaurateurs, retailers, and a strong sense of history and placemaking at the town square. From this initial foundation, more housing will be built through adaptive reuse and ground-up development. Ultimately, the multi-decade goal is a large startup district that encompasses over 100,000 square feet of creative spaces across many historic buildings, over 1,000 apartment units, dozens of food and beverage options, great shops, and an incredible sense of place where Atlanta was literally founded—and now, a district for founders and startups.

After last week’s post announcing the new Atlanta Tech Village location in downtown Atlanta, the most common question and refrain that I heard from others is, “Why downtown?” Like many of my fellow Atlantans, I’ve historically avoided downtown, other than going to the occasional corporate or sporting event. Like many downtowns around the country, ours has struggled for many years but was serviceable until Covid hit and dramatically altered the landscape. The last 10+ years in Atlanta have really opened my eyes to how regions of the city can be dramatically upgraded and enhanced, with the two biggest makeovers being Midtown Atlanta and the Beltline. After $10 billion plus of investment in each of those areas, the number of residential units, restaurants, retailers, and overall walkability and livability of those areas have skyrocketed. When friends come to town now, the first thing I want to show them is the incredible development on the Beltline around Ponce City Market and Krog St Market, especially how Atlanta is making important steps for areas of the city to be truly walkable, something that’s always been a nagging challenge for the region.

Now, while the Beltline and Midtown revitalization have achieved extraordinary results, I hadn’t spent any time studying or thinking about downtown Atlanta. On the surface, it seems like downtown Atlanta as a live-work-play region would be a no-brainer infrastructure-wise. There are a large number of subway stations, three interstates that touch it, and miles of dedicated bike lanes. There’s a historic grid laid out in the early 1840s that is walkable, fairly flat, and easy to get around. From an entertainment point of view, it’s the home of the Atlanta Falcons NFL team, the Atlanta United MLS team, and the Atlanta Hawks NBA team. In addition, there are hundreds of concerts and entertainers every year that come through downtown at State Farm Arena, Mercedes-Benz Stadium, the Tabernacle, Rialto, and multiple music venues at Underground Atlanta. Based on the raw number of concerts alone, downtown is easily the live music capital of Atlanta. Finally, the Georgia World Congress Center is the fourth largest convention center in the country, and downtown has over 14,000 hotel rooms along with the 22-acre Centennial Olympic Park, Georgia Aquarium, College Football Hall of Fame, Center for Civil and Human Rights, World of Coca-Cola, and much more. Again, downtown should be a successful, thriving heart of Atlanta.

Only there are a number of challenges that have to be overcome for downtown to live up to its potential. The first challenge is that there are very limited residential options. Downtown was built as the central business district and has 15+ million square feet of office space, and unfortunately, most of it was built between the 1960s and 1980s in the John Portman style such that the buildings are cordoned off from the street in a cloister garden format and create a harsh environment when not inside the structure. Because of these large floor plates, the buildings are not convertible to residential. With the work-from-home and remote work trends, there are a handful of condo and apartment buildings, including some historic ones that have been converted over the years. Going forward, downtown needs to become a residential neighborhood, and thousands of new residential units need to be built or converted from the office buildings conducive to conversion.

The second challenge is that downtown has an overabundance of parking lots and parking decks. There is too much parking. This manifests itself in poor land use where a lack of density hurts the neighborhood. It’s also challenging in that most of these parking decks and parking lots act as a covered land play where there’s no need or impetus to sell because the property values are so low, and only a modest amount of parking rental income will more than cover the annual costs. In addition, many of these parking lots and parking decks have been owned by families for generations, and their basis is so low that they’re better off just not doing anything versus helping contribute to the revitalization of downtown.

The third challenge is the doom loop in the emptying out of the office buildings and how that then translates into the local restaurants, dry cleaners, and other service businesses going out of business. Then, when those buildings are sold at dramatically lower prices, the property taxes decrease, and the city and county have fewer funds to work with to help the neighborhood. This downward spiral continues indefinitely. With 15+ million square feet of office space, it’s hard to see the office market downtown thriving anytime soon. Even if you buy a building at a dramatically lower rate to modernize it and make it attractive for tenants, it’s going to cost $200 dollars per square foot to renovate. If you buy a 100,000 square-foot building for $100 a foot ($10 million), just to make it attractive and make it desirable space, it’s going to cost another $20 million to upgrade it, and now you’re at $300 a foot, and the market will not bear that for many years.

The fourth challenge, and ultimately the number one challenge, is the centralization of homeless services in the region in downtown. This is exacerbated by the unofficial homeless support services that create an environment whereby multiple times a day and in multiple parts of downtown, it looks like a refugee camp with so many people waiting in line for food and general help. It really is heartbreaking. Outside of those periods of time for services, the concentration of homeless services in downtown also results in hundreds, if not thousands, of voluntarily homeless people. A voluntarily homeless person is somebody who refuses services from the faith community, the nonprofits, and the government. Voluntary homelessness is downtown’s most pressing and most obvious issue with no easy solution.

On the momentum side, there are a number of excellent things happening in downtown right now. Number one is Georgia State’s continued investment in the community with the announcement of their Blue Line, similar to a Beltline-type experience. Georgia State is building out a series of paths throughout the urban campus focused on safety, security, eyes on the street, and everything else you would want in a great college experience. Georgia State is the largest university in Georgia.

The second item on the momentum front is the funding of the Stitch, whereby an initial 4.5 acres of current interstate will be covered with a new park right in the northern part of downtown, and that project is scheduled to begin in the next few years. More parks and plazas will spur development in the area.

The third item on the momentum front is the continued investment in government-sponsored affordable housing through 2 Peachtree St. and a number of related initiatives. The main idea is to combine a number of different government programs and grants to put a capital stack together to convert some of the buildings, as well as build new housing near Five Points MARTA station.

The fourth item on the momentum front is Centennial Yards building a major development in the Gulch, with two 18-story towers halfway done already, and breaking ground on a new entertainment district that will be nearly 500,000 square feet, including the new Cosm 5,000-seat concert venue adjacent to Mercedes-Benz Stadium and State Farm Arena.

Ultimately, downtown Atlanta is the front door to all of Atlanta. Between the corporate events, the convention center, the stadiums, the concert venues, the hotels, and museums, over 50 million visitors per year come to downtown Atlanta. Downtown is the first and only impression of Atlanta for many guests. We chose to put our second Atlanta Tech Village location in South Downtown not because it was the easy thing to do but because it was the right thing to do. Downtown needs entrepreneurship and innovation. Downtown is struggling, and Atlanta has been and always will be led by entrepreneurs, business leaders, and civic leaders. Atlanta Tech Village is going downtown because it’s the biggest challenge and the biggest opportunity to help entrepreneurs and Atlanta.

Last week, we announced the groundbreaking for the new Atlanta Tech Village in South Downtown Atlanta. After starting the Atlanta Tech Village in late 2012, one of the most popular questions I heard was, “When are you going to open a second location?” Back then, we were learning the ins and outs of building community and running a co-working facility. After doing it for a few years and feeling like we understood more, we did peek around at other buildings only to find that the real estate market was white hot, and real estate prices had significantly outpaced the rents chargeable to startups. My answer to the question was simply that it was a one-and-done; no new locations because the math didn’t make sense. Fast forward over a decade, and we just broke ground on our second location in South Downtown Atlanta (Instagram, LinkedIn).

Anyone who’s been to downtown Atlanta knows that there are a variety of challenges and opportunities. Much like what has been covered in the news over the last year around doom loops in cities across the United States, downtown Atlanta has been hit particularly hard. Put simply, a doom loop is when office buildings start to empty out due to work-from-home and remote work. When office workers don’t come in, service businesses in the neighborhood, like restaurants and dry cleaners, go out of business as well. This then hurts property values, such that fewer property tax dollars are generated resulting in fewer city services, and this doom loop continues in a downward spiral.

In October of last year (2023), I was at a Metro Atlanta Chamber executive committee meeting. After the meeting, I was catching up with some friends, one of whom runs the largest commercial office space landlord in Atlanta. We were talking about what’s going to happen with all this empty commercial real estate and how it’s going to play out across the country, but especially in Atlanta. He then shared with me that the developer in South Downtown Atlanta, Newport, had just had all 53 buildings and 10 city blocks in their portfolio go into foreclosure. I had read about this project over the years and even been presented it back in 2018 as a potential location for a second Atlanta Tech Village location, but I had never visited it, nor had I studied it closely. After the meeting, I went back to my laptop and dove into learning as much as I could about anything and everything related to the South Downtown Atlanta redevelopment. The most eye-opening thing to me was how there is this incredible collection of historic buildings literally in the neighborhood where Atlanta was founded, and due to a variety of reasons, they were nearly untouched, like a beautiful time capsule.

After getting a better feel for it, I reached out to some friends to get feedback and ideas on what it would be like to build an entire tech startup innovation district, taking many of the concepts that we developed over 10+ years at Atlanta Tech Village and applying them to an entire neighborhood across 50+ buildings. It was not too dissimilar from having our own college campus, only the campus is adjacent to Mercedes-Benz Stadium, State Farm Arena, the newly announced Cosm concert venue, the State of Georgia Capitol, City of Atlanta City Hall, the largest university in the state in Georgia State University, and the busiest train station in Metro Atlanta, Five Points MARTA. As the idea started to crystallize, the obvious next step was to go down and see it in person, to walk the buildings, and to feel the history and the culture of the heart of Atlanta.

I reached out to a friend who knew the neighborhood well and the Newport team for a tour. Seven or eight of us showed up, not knowing what to expect, and proceeded to spend the next six hours walking through amazing buildings, going up on rooftop patios, looking out over the city, rummaging around old department stores, and imagining what could be in the most walkable city blocks in the region nestled between multiple train stations and three interstates. After going through building after building, it became apparent that this truly was a once-in-a-lifetime opportunity to build an entire neighborhood dedicated to helping entrepreneurs succeed. From the living quarters in great historic buildings to all the transit opportunities, beautiful loft office spaces, and one of the biggest entertainment districts in the country, it was clear there was something unbelievably special in South Downtown Atlanta.

After buying the properties, mostly through foreclosure and deed in lieu of foreclosure, in December of last year and January of this year, we immediately set to work on a grand plan for the neighborhood, with the Atlanta Tech Village as the center of it (fun Atlanta Magazine story). Now, six months later, we’ve broken ground on the new Atlanta Tech Village downtown location set in a beautiful historic hotel from 1909 called the Sylvan Hotel, atop an incredible retail space that was the Imperial Fruit Co (a postcard company!) for many years on historic Hotel Row adjacent to Mercedes-Benz Stadium, host of the 2026 World Cup.

The vision for the neighborhood is to be the number one place for entrepreneurs to go to succeed. Through a combination of living laboratory, where entrepreneurs help each other, and the greater community through mentors, business leaders, and civic leaders work together to grow our startup community. We will open the new Atlanta Tech Village location early next year (2025) while renovating the majority of the neighborhood for our grand opening on a larger scale during the 2026 World Cup, complete with multiple ATV-themed locations spread throughout.

Of course, we need help. We need pioneers who want to see a thriving downtown Atlanta, full of entrepreneurs and startups inventing the future. We need mentors and coaches helping these entrepreneurs put their stamp on the city. We need investors funding the next generation of innovation. We need restaurateurs and retailers to fill up the historic store fronts. We need business leaders supporting downtown.

In the most recent episode of Acquired, Ben Gilbert and David Rosenthal interview Howard Schultz, the founder of Starbucks. It’s an excellent, wide-ranging show with many incredible takeaways. One anecdote that stood out occurs at the 57-minute mark when Ben and David ask Howard about his two key leaders. Howard shares that every single Monday night for ten straight years, the three of them had dinner together.

There’s so much power in the value of long conversations about what’s going on, what’s working well, and what’s not. This allows for alignment, the ability to disagree and commit, and a general mind meld among founders. Much of this happens organically, especially in the earliest days when everyone is in the same office together, checking in daily through stand-ups and regular meetings. However, as the business grows, it becomes harder and harder due to more requests for your time, more travel, more issues, and more team members. These increased demands on the founding team make it even more valuable to have a regular, unscripted, long chunk of time to get together without the distractions of the office and day-to-day tasks.

At Pardot, we did this for many years as our monthly strategy dinner. On the first Wednesday of every month, the leadership team would get together for a 3+ hour dinner. During dinner, we would go over anything and everything, focusing primarily on the harder, more strategic topics that needed more time to flesh out. Regular tactical items were addressed in our daily and weekly meetings. Anytime we had an issue that was too large or strategic but not urgent, we would put it in a Google Doc and then address whatever was in the Google Doc at the monthly strategy dinner.

At SalesLoft, a few years in, as the business was scaling, we did the same thing—a monthly strategy dinner with the executive team where we hashed out the most important topics. I vividly remember sitting at Maggiano’s, debating substantial pricing and packaging changes to the software, and dealing with so much complexity, edge cases, and customer anecdotes. Having these intense conversations helped everyone be heard, but more importantly, it helped us arrive at the best decision. We were much better off as a company and organization with these monthly strategic dinners.

My recommendation to entrepreneurs is to establish a regular dinner or offsite with the exec team where parking lot items and big topics are debated. This isn’t an exercise in consensus building; it is an exercise in laying everything out, making sure everyone’s heard, and having a leader make a decision.

Last week, I was talking to an entrepreneur who was contemplating a major business change. The conversation reminded me of the early days of Pardot. Back then, the product was primarily forms and landing pages with CRM integration. Anything related to email marketing was done through API calls to other systems like MailChimp or Constant Contact. Products that we take for granted today, like Twilio, to abstract out the email component of a system, did not exist.

We had a large number of debates around whether or not we should become an email service provider. To be an email service provider would require a major business change, whereby we allocated our limited resources to things like managing email servers, working with different email infrastructure and inbox companies like Gmail and Outlook on deliverability, and adding more complexity to our onboarding program with customers as they now had more technical changes to make. It wasn’t a decision to be taken lightly.

After going back and forth and thinking about it from first principles around delivering the best solution to our customers, delivering a solution that was the most seamless, and delivering a solution that helped customers generate the best return on investment, we made the decision to become an email service provider. While it was painful in a few areas, especially around deliverability and reaching inboxes, overall, it was an incredibly important and valuable change to the business. We could now deliver a better solution, both triggering emails instantly as well as sending bulk emails like company newsletters natively within the software.

In terms of customers, they already had budgets for email marketing platforms, and so it also made it easier in the sales cycle because we could now replace their email marketing product with our marketing automation system. Business marketers wanted to run more advanced online marketing campaigns, and now they could do it in a more dynamic and productive way.

Contemplating a major business model change that involves more staffing, more technology, and more unknowns can be unnerving. For us, while it added more complexity to become a full email service provider, it was one of the best decisions we ever made. We made it through the learning curve and ultimately delivered a much better solution to customers.

Last week, I was listening to an entrepreneur who shared that he likes processes much more than goals. This concept rings true with me as well. Goals are important because they help us focus on where we’re going and how we’re measured (especially SMART goals). However, it is much more important to spend time on the process, especially the processes within your control, that will ultimately help you achieve those goals.

Let’s take a simple example: sales. Suppose you have a startup, and your goal is to generate $1 million in new revenue this year. Typically, you would divide this into quarters, potentially incorporating seasonality, and set a goal to sell $250,000 each quarter. At the end of the year, you would add up the quarterly sales and compare them to the annual goal of $1 million to assess performance. This approach has value and is necessary, but it is much more important to focus on the process and ensure it results in the desired goal.

For this sales example, the process would involve the number of cold calls made per day, the number of emails sent, the number of meetings scheduled, the number of meetings attended, the number of proposals sent, the number of proposals moved to the next stage, and the number of proposals closed as deals, and so on. It starts with the things that are within your control. If I need to make 50 cold calls a day to achieve a certain number of demos, proposals, and deals, it is 100% within my control to make those calls. If I need to attend two tradeshows a month and talk to 100 people at each tradeshow, that’s within my control. The process needs to be the focus, knowing that you have designed and organized a process that allows you to achieve your goals.

Over the years, I’ve seen many entrepreneurs set goals without having the underlying process. Even if they did, the process might not have been feasible to achieve those goals. Common examples include wanting to sign up 10,000 users for a product or wanting to raise $5 million in venture capital. These could be reasonable goals, but without a clear process leading to the outcome, it’s hard to know if these are worthwhile and achievable goals.

Two ways to approach this are top-down and bottom-up. The top-down approach involves setting a goal, such as signing up 10,000 users, and then working backward to develop a process to achieve it. You then assess whether that process is reasonable, feasible, and financially viable. The bottom-up approach starts with identifying a reasonable process at the current time and for a given duration. You then estimate how many users you can sign up per day, week, or month with this process. At the end of the year, you can achieve a certain number of users. This method involves starting with a process that works today, understanding the current outcome, extrapolating that over time, and then setting a goal based on that outcome. In the first example, we pick a goal and try to work backward with a process to achieve it. In the second example, we start with the process, evaluate the likely outcome, and then set a goal based on that outcome over a period of time.

Entrepreneurs would do well think process first, goals second. Goals are important and part of achieving great things, but a process that is within your control is more important. Continually refine the processes and ensure the outcomes are aligned with the goals.